Aaj mere paas paisa hai, bangla hai, gaadi hai, naukar hai, bank balance hai, aur tumhare paas kya hai? asks Amitabh Bachchan, addressing his brother Shashi Kapoor in the iconic film Deewaar released in 1975.

He was showing off his possessions, considered a barometer of success. More than four decades later, the society still evaluates the success of a person by the real assets he possesses.

Among all the assets, a house is typically the leading parameter by which a person’s success is measured, especially in India.

“Antilia”, the house where India’s richest person Mukesh Ambani lives is deemed to be the world’s most expensive residential property owned by an individual. If you type Ambani on Google, the first option that the search engine automatically suggests is “Ambani House”, (The next suggestion incidentally is Ambani Daughter wedding) which shows people are interested to know about it more than anything else associated with Ambani, who is the chairman of Reliance Industries Ltd, the biggest company in India.

Most people who aspire to buy a house of their own are deterred by high prices. Over the last four to five years, real estate has also given negative returns in most cases when adjusted with inflation.

However, Your mother is pestering you. Your friends are buying homes. And you’re wondering if you should stop renting and buy a house too. Your pet wants a yard, your kids want a playground, your wife wants her kitchen garden, and you wouldn’t mind a garage and an office den.

There’s only one problem: You aren’t sure you can afford it. Your house is likely to be the biggest purchase you will make in your life, and you may spend years paying for it.

While buying a home is often referred to as the ultimate Dream, remember that your Home Is Not an Investment. Appreciation in price, if any, of your residential house is just an incidental advantage as ideally you are never going to sell it.

If you buy before you are ready, there can be major financial consequences. For one, if you overspend, you can become house poor.

You should be sure you are ready and aren’t just buying because it’s what you are expected to do, or it’s the next step or because of family pressure.

Do you want to commit yourself to a mortgage payment for the next 10 or 15 years?

It is important to buy a home for the right reasons.

“Wanting” to buy a home and “being ready” to buy a home are two completely different things.

A recent study found that 56 percent of Millennials believe owning a home is more important than paying off debt or retiring comfortably. As per the study, the average age of buying a home has come down from 35 to as low as 26. The problem is the young are committing themselves to a long term mortgage very early on in their careers.

They may want to or are buying a home but they might not be ready for it.

Should You Buy a House?

Owning your own home is everyone’s Dream. There’s no doubt that having your own address comes with a lot of satisfaction and pride; it also comes with plenty of extra costs and maintenance. That’s why you want to be absolutely certain you’re ready to buy a house.

How do you know you’re ready?

If you can answer yesto the following questions, you’re prepared to take the plunge.

Are you out of debt?

Before you take on a major housing loan, you should have no student loans, no vehicle loans, no credit card debt and no consumer debt.

Do you have an emergency fund with six months of expenses saved?

If you got laid off today, could you pay your installment and your bills for at least six months while looking for work?

Do you have enough cash for a 25% down payment on a 10/15 year loan

You can negotiate for a better rate and settle for a lesser repayment period. Remember initially in an EMI, you are just paying mainly interest and only later does the principle start getting paid.

Will your EMI be 25% or less of your monthly take-home income?

This shall leave you plenty of room in your budget to achieve other goals, like saving for retirement and putting money aside for your kids’ education or planning that holiday apart from the mundane, Roti, Kapda & Makaan.

The Stability of Your Financial Future

This is another important factor when determining whether you should buy a house now or wait until the future. If you have recently changed jobs or started a new venture, if you are thinking about changing jobs, or if you are expecting any major changes to your income, it is not a good idea to buy a house until you are on more solid footing. Banks and Home Loan providers typically require you to have been with your employer for at least a year or two before they will consider you for a loan.

Furthermore, you need to have a plan to pay your loan in the event that something does go wrong in the future, such as a layoff or a medical problem or any other emergency.

Have you considered your other short term goals

Re think your short-term goals that you may have and think about how it may impact EMI payments. Say, having a new born may change priorities and that may impact income of the household. However, the home loan EMIs will continue to accrue; you may move from a Double income to single income with a higher expense level too. The first thing you need to do is to estimate the liquidity, contingency and funds for near-term goals. Make a list of your expenses-both monthly and annual. Also, note down the near term (up to 3-5 years) goals and funds you need for these goals.

Do you plan to stay in the same location for more than five to seven years?

Are you settled in your job or career, Will your Children’s education force you to move to another location, is this address your final destination? These are the other factors to consider before finalizing on buying a house.

The Current Real Estate and Credit Market

While this factor may not be as crucial as the other considerations, you still need to consider it. Look at the current interest rates, and consider the experts’ opinions as to whether property values are on the rise, or are likely to fall.

If interest rates are at record lows, it may be a good time to buy, as you will pay a reduced cost for the privilege of borrowing money.

If property values are on the decline, it may be a good time to wait as you could end up getting a better deal on the same type of home in just a few months’ time.

It can be very hard to accurately predict what interest rates or property values will do, so these shouldn’t be deciding factors – but they are still worth considering.

Your Commitment to Home Ownership

Being a homeowner is different than being a tenant. You need to take care of all of your own home repairs and maintenance, rather than counting on someone else to do it. You may have more yard work, as well as additional responsibilities that tenants don’t have to worry about. Also factor in the property taxes, RWA expenses & contributions etc in your costs.

While some people don’t mind such chores, others don’t want the hassle. Consider whether you are ready to take on these added responsibilities of home ownership before you make your decision.

What does the family feel about buying a home?

Owning your own home does give the owner and their family a sense of security and stability, but make sure everyone in your family is on board with the decision. Is it only your priority and choice or does the entire family, especially your spouse, feel as passionately about buying a house at this juncture. Is the neighborhood, size of the house etc acceptable to all. Are they willing to compromise on other short term goals to make this purchase.

If your answer is noto any of the above questions, now may not be the right time for you to buy a house. Put your home purchase on hold and focus on your finances until you can answer yesto all of these questions.

Everyone gets to the point where they want stability in their lives. Owning your own home gives you a set neighborhood, schools and community that you can call your own.

Experts consider 35plus as the ideal age to buy a home, an age when one has accumulated at least 30-40 per cent for the down-payment, when the career has stabilised, children have started middle school and you have the ability to pay regular EMIs.

But, buying a house shouldn’t come at the cost of other important goals like your child’s education and your own retirement, neither should it impact your lifestyle significantly. Home loan EMI is one of the biggest breakers of passions such as travel, entrepreneurship and other interests. Buying a home should not mean having to work in a highly unsatisfying job or missing out on investing for your kids only because of the EMI pressure. It can also set off your time to retirement by a large number of years.

Unlike financial assets that are liquid-you can redeem your mutual fund units and realize the money in a few days-real estate is not liquid. It can take days to months to find a buyer and the ensuing hassle to sell off the property really makes it a sticky asset.

The recession of 2008 resulted in a record number of mortgage foreclosures in the US. More than Three million Americans foreclosed upon their home in 2008, an 81 percent increase from the previous year and a 225 percent increase from 2006. The post-recession economic climate (among other factors) contributed to the delay of younger Americans becoming first-time homeowners. Despite the delay, a majority of Millenials still view owning as a superior option to renting due to emotional reasons.

As a part of the decision making process, lets also consider

Real Estate Vs Equity, purely as an investment

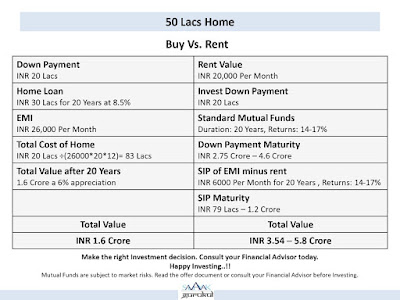

Lets evaluate the decision if it was to be made purely on economic factors of Buy vs Rent.

A friend bought a property for Rs 30 lakhs in Mid 2002. He sold the property at Rs 1.5 Crores in 2018– a profit of Rs 1.2 Crores on an investment of Rs 30 lakhs. Many of my other friends were super impressed with the profits, which this friend made – but I was not as impressed as my other friends.

Let me explain why: While this friend’s absolute returns were good, Lets use a metric known as Compounded Annual Growth Rate (CAGR) to evaluate the performance of investments. The CAGR of my friend’s investment was 10.6%. While this was more than returns from FD or other risk free investments, top performing diversified equity mutual funds over the last 15 years have given more 15% CAGR returns. If he had invested in Equity Mutual Fund, Rs 30 lakh would have grown to Rs 2.44 crore @ 15% CAGR over 16 years.

If he had invested Rs 30 lakh as a Lump sum amount in HDFC EQUITY FUND on 25-01-2002 ( NAV Rs 19.47), Today the Current Value( As on 22ndJan, 2019) of his Fund would have been Rs 9.69 crore (NAV Rs 629.47).

That is the power of Equity Mutual Fund and the kind of growth you can expect. ( And we have still not considered the taxation aspect which is only 10% on LTCG in Mutual Funds)

Give maximum time to your investment to get the most out of power of Compounding.

In 15 years from 2001 to 2016, 45 equity mutual funds have multiplied the investor wealth more than 25 times. In fact Reliance Growth Fund & Franklin India Prima Fund grew by more than 50 times.

This growth came in one of the most volatile periods in the Indian Stock Market history, a period which saw six major corrections of more than 20% and a crash of more than 60% in 2008.

Those who had the conviction & stayed invested whether through SIP or lump sum generated tremendous amount of Wealth in this period.

It goes without saying that nothing can beat Equity in terms of returns in the long term.

The other qualitative parameter comparisons are also outlined below for your ready reference:

I shall like to leave you with a final thought, Warren Buffet, one of the richest man in the world and a marqee investor, lives in a quiet neighborhood of Omaha, Nebraska in a house he bought in 1958 that is today worth 0.001% or less of his total wealth.

Thus, use the above parameters to finalise on this most important financial decision. Discuss it with your family, do your research, Consult your financial advisor, study the real estate market, or consult an expert and only then decide whether, Should you buy a house?

Happy Investing!

Stay Blessed Forever!

Sandeep Sahni

You may contact us at:

91-9888220088, 9814112988

sandeepsahni@sahayakassociates.com,

Follow us on:

www.facebook.com/sahayakassociates,

www.twitter.com/sahayakassociat,

Note: All information provided in this blog is for educational purposes only. They don’t constitute any professional advise or service. Readers are requested to consult a financial advisor before investing as investments are subject to Market Risks.